Table of Contents

Introduction

Internal audit of Order to Cash is essential to identify potential risks, strengthen controls, and enhance the overall financial health of the organization. In this comprehensive guide, we will explore the various facets of the Internal Audit of Order to Cash, discussing the strategic importance, components, risks, controls, entity-level controls, key performance indicators (KPIs), dashboards, checklists, fraud detection techniques, and conclude with valuable bonus tips for internal auditors. Dive into the critical processes that ensure your business’s revenue stream and customer satisfaction

Internal audit of Order to Cash cycle is essential to identify potential risks, strengthen controls, and enhance the overall financial health of the organization. In this comprehensive guide, we will explore the various facets of the O2C cycle and discuss the strategic importance, components, risks, controls, entity-level controls, key performance indicators (KPIs), dashboards, checklists, fraud detection techniques, and conclude with valuable bonus tips for internal auditors.

The Order-to-Cash cycle, often abbreviated as O2C or OTC, is a series of interrelated business processes that begins with a customer placing an order and concludes with the receipt of payment. This cycle plays a pivotal role in the smooth operation and financial sustainability of an organization.

Strategic Importance of the O2C Process

The Order-to-Cash cycle is strategically vital for businesses for several reasons:

- Revenue Generation: The O2C process directly impacts an organization’s revenue stream. Efficient handling of orders, invoicing, and collections ensures a steady cash flow.

- Customer Satisfaction: A well-managed O2C process leads to satisfied customers who receive their orders promptly and experience seamless billing and payment procedures.

- Cost Control: Effective control of the O2C cycle minimizes operational costs, such as inventory carrying costs and collection expenses.

- Data Insight: The O2C cycle generates a wealth of data that can be analyzed to gain insights into customer behavior, market trends, and performance indicators.

- Regulatory Compliance: Compliance with accounting and tax regulations is dependent on the accuracy and transparency of the O2C process.

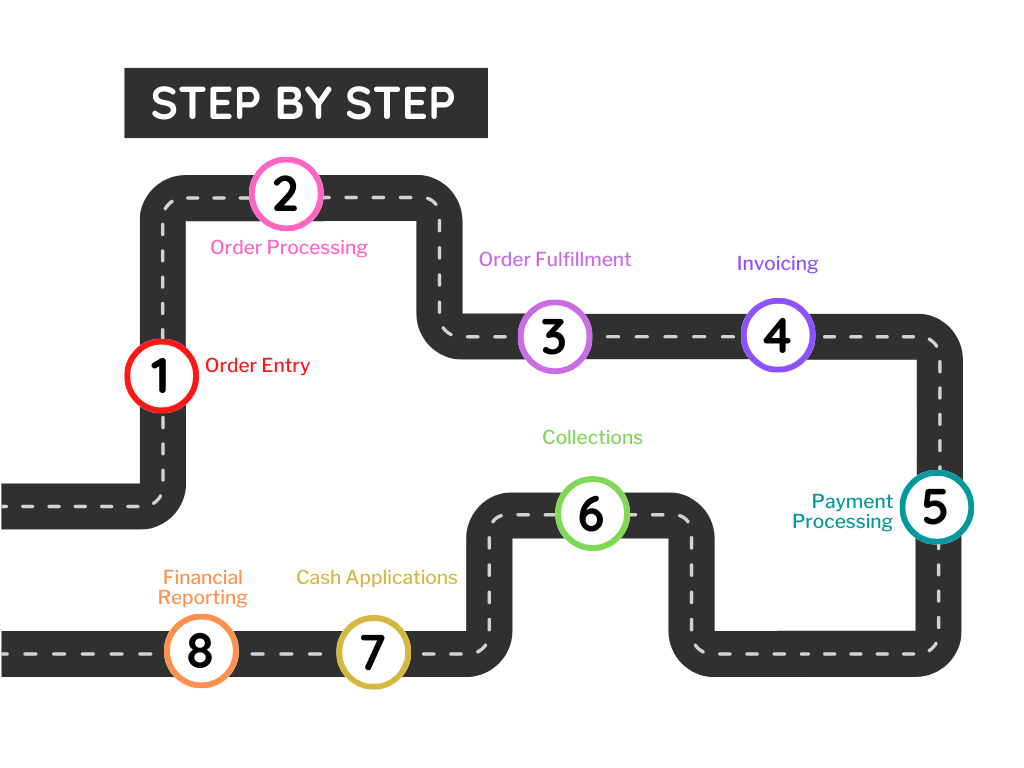

Components of Order to Cash Cycle

The O2C cycle consists of several interlinked components, each playing a crucial role in the overall process:

- Order Entry: The initial step involves capturing the customer’s order, which can be initiated through various channels such as sales representatives, e-commerce platforms, or phone orders.

- Order Processing: Once an order is received, it is processed to ensure that the organization can fulfill it. This stage involves checking inventory levels, lead times, and production capacity.

- Order Fulfillment: This phase includes the actual delivery of goods or services to the customer. It may involve shipping, warehousing, and manufacturing activities.

- Invoicing: Invoicing is the documentation of the transaction, detailing the products or services delivered, their prices, and payment terms. Accurate and timely invoicing is crucial to cash flow.

- Payment Processing: This step involves receiving and processing payments from customers through various payment methods, such as checks, credit cards, or electronic transfers.

- Collections: In cases of delayed or incomplete payments, organizations may engage in collections activities to recover outstanding amounts.

- Cash Application: Payment receipts are matched and applied to the corresponding customer accounts to ensure accurate financial records.

- Financial Reporting: This component involves the preparation of financial statements and reports, which are essential for management, investors, and regulatory compliance.

Potential Risks and Controls in the Order to Cash (O2C) Cycle

Each stage of the O2C cycle presents unique risks that require specific controls to mitigate them. Let’s examine potential risks and corresponding controls at each stage:

| Stage | Risks | Controls |

| 1. Order Entry | – Inaccurate or incomplete order information. – Unauthorized or fraudulent orders. | – Implement order validation checks to ensure accuracy. – Use authorization protocols for order processing. |

| 2. Order Processing | – Overpromising delivery times. – Errors in order data entry. | – Maintain clear communication between sales and operations. – Implement data validation and verification processes. |

| 3. Order Fulfilment | – Incorrect or damaged product shipments. – Delays in product delivery. | – Quality control checks before shipping. – Monitoring and reporting delivery performance. |

| 4. Invoicing | – Incorrect pricing or discounts. – Invoices not reaching the customer. | – Automated pricing and discount validation. – Implement invoice tracking and confirmation processes. |

| 5. Payment Processing | – Misapplied payments. – Payment fraud. | – Automated reconciliation processes. – Implement payment security measures. |

| 6. Collections | – Poor communication with delinquent customers. – Legal and compliance issues. | – Clearly defined collection policies. – Legal compliance and documentation processes. |

| 7. Cash Application | – Misallocation of payments. – Data entry errors. | – Automated payment matching and reconciliation. – Data verification processes. |

| 8. Financial Reporting | – Inaccurate financial statements. – Non-compliance with accounting standards. | – Regular reconciliations and audits. – Strong internal control systems. |

Entity Level Controls in the O2C Cycle

Entity level controls are overarching controls that influence the effectiveness of an organization’s internal control system. In the context of the O2C cycle, they include:

- Tone at the Top: The commitment to ethical behavior and financial integrity starts with senior management. They set the tone and establish the culture of compliance and accountability.

- Policies and Procedures: Written policies and procedures governing the O2C cycle should be in place. These documents provide guidance on how transactions should be conducted, documented, and reported.

- Segregation of Duties: Assign responsibilities and authorities in a way that prevents a single individual from having too much control over the process. This segregation helps prevent fraud and errors.

- Training and Awareness: Ensure that employees involved in the O2C process receive proper training on controls, compliance, and ethical behavior. Regular awareness programs can help reinforce these principles.

- Monitoring and Auditing: Implement ongoing monitoring and periodic audits of the O2C cycle to identify issues, fraud, or compliance violations. These audits may be internal or external.

- IT Controls: Implement controls within the organization’s IT systems to secure data, prevent unauthorized access, and ensure the accuracy and integrity of financial data.

Key Performance Indicators (KPIs) in the O2C Cycle

To assess the effectiveness and efficiency of the Order-to-Cash, organizations rely on key performance indicators (KPIs). These metrics help internal auditors and management monitor the health of the O2C process. Here are some essential KPIs:

- Days Sales Outstanding (DSO): DSO measures the average number of days it takes to collect payment after a sale. A lower DSO indicates a more efficient cash collection process.

- Order Accuracy: This KPI measures the percentage of error-free orders processed. High order accuracy reflects strong order entry and processing controls.

- Invoice Accuracy: The percentage of invoices that are error-free is a key indicator of the accuracy of the invoicing process.

- Collection Effectiveness Index (CEI): CEI measures the success of the collections process in recovering outstanding payments.

- Bad Debt Percentage: This KPI tracks the percentage of unpaid invoices that are unlikely to be collected. High bad debt percentages may indicate issues with credit policies.

- Credit Limit Adherence: This metric measures the extent to which customers adhere to their credit limits. High deviations may signal credit risk.

- Customer Satisfaction: Customer feedback and satisfaction scores provide insights into the quality of the O2C cycle from the customer’s perspective.

Dashboard in the Order to Cash Process

Dashboards are invaluable tools for internal auditors to monitor and assess the O2C process. An O2C dashboard should include:

- Revenue Metrics: Track revenue trends, revenue sources, and forecasts to understand the financial health of the organization.

- Cash Flow: Monitor cash flow and liquidity, identifying any areas where cash may be tied up or potential cash shortages.

- Collection Performance: Display key collection KPIs, such as DSO, CEI, and bad debt percentage, to assess the effectiveness of collections efforts.

- Invoice Status: Keep an eye on the status of invoices, including those outstanding, paid, or disputed.

- Customer Behavior: Analyze customer payment patterns and identify high-risk customers or those who consistently pay late.

- Order Fulfillment: Monitor order fulfillment rates and the time it takes to process and deliver orders.

- Compliance and Risk: Highlight potential compliance issues and risks within the O2C process.

Checklist for Internal Audit of Order to Cash

Internal auditors should utilize a checklist when conducting an audit of the O2C cycle to ensure a thorough and systematic review. Here’s a sample checklist:

- Review the O2C process flow and documentation.

- Evaluate the accuracy and completeness of customer orders.

- Assess the effectiveness of order processing controls.

- Review the accuracy of invoicing and adherence to pricing policies.

- Examine the security of payment processing and cash handling.

- Evaluate the collections process and its efficiency.

- Ensure proper allocation of cash receipts to customer accounts.

- Review financial reporting and compliance with accounting standards.

- Assess entity-level controls and their implementation.

- Verify IT controls and data security measures.

- Analyze KPIs to identify performance issues or trends.

- Check the effectiveness of customer communication and dispute resolution.

- Assess the quality of customer credit policies.

- Review customer satisfaction feedback and the resolution of customer issues.

- Identify any potential fraud risks or anomalies.

Techniques for Detecting Fraud in the Order to Cash Process

Internal auditors play a crucial role in detecting fraud within the O2C process. Several techniques and red flags can help auditors identify potential fraud:

- Anomalies in Order Patterns: Look for unusual order patterns, such as excessive returns, order cancellations, or multiple orders from the same customer.

- Invoice Manipulation: Scrutinize invoices for unusual pricing, unauthorized discounts, or alterations in payment terms.

- Payment Irregularities: Identify irregularities in payment receipts, such as payments from unusual sources or payments not matching outstanding invoices.

- Duplicate Payments: Review payment records for duplicate payments made by the same customer.

- Unauthorized Discounts: Watch for unauthorized or excessive discounts granted to customers, which may indicate collusion between employees and customers.

- Altered Sales Orders: Examine sales orders for alterations or unauthorized changes, which can lead to fraudulent orders.

- Fake Customers: Verify the existence of new customers and their creditworthiness, as fake customers may be created to facilitate fraudulent transactions.

- False Returns: Investigate returns that appear excessive or that lack proper documentation.

- Collusion: Pay attention to signs of collusion between employees and external parties, such as customers, to commit fraud.

- Late Revenue Recognition: Review the timing of revenue recognition to ensure it complies with accounting standards and is not manipulated to inflate financial results

Bonus Tip for Internal Audit of Order to Cash

Staying updated with the latest industry trends, emerging technologies, and regulatory changes is essential for internal auditors. Continual professional development and networking within the audit community can provide valuable insights and resources for a successful audit of the O2C cycle. Additionally, fostering effective communication with business units and stakeholders can help auditors build strong working relationships and facilitate smoother audits. Remember, the role of an internal auditor goes beyond detecting problems; it also involves suggesting improvements and assisting in their implementation to enhance the organization’s overall performance.

Conclusion

The Order to Cash cycle is a cornerstone of an organization’s financial health and customer satisfaction. Proper management and internal auditing of this cycle are essential to ensure that orders are efficiently processed, payments are collected on time, and financial data is accurate. In this comprehensive guide, we’ve explored the strategic importance of the O2C process, its components, potential risks and controls, entity-level controls, key performance indicators, dashboards, checklists, fraud detection techniques, and bonus tips for internal auditors.

As businesses continue to evolve, internal auditors must adapt and stay informed about emerging risks and best practices. By conducting thorough and systematic audits of the O2C cycle, organizations can enhance their financial performance, mitigate risks, and maintain the trust of their customers and stakeholders.

Read basics of Internal Audit from my previous blog

For other resources you can visit website The Institute of Internal Auditors

Thank you for reading and stay blessed.

1 thought on “Internal Audit of Order to Cash | Comprehensive Guide 2024 (Updated)”